Income-producing assets stand out as a fundamental strategy for investors worldwide who seek financial freedom and wealth building. Including stocks, bonds, real estate, certificates of deposit (CDs), and online businesses, income producing assets offer a diversified approach to earning potential beyond conventional employment or business income.

The role of income-producing assets in wealth accumulation is undeniable. Not only does it offer a mechanism for generating steady and passive income, but it also helps safeguard against inflation and economic downturns if you choose to implement asset diversification. However, it is not a guarantee against inflation or economic downturns.

One should note that economic cycles, technological advancements, and global events significantly influence the performance and viability of income-producing assets. As such, investors should remain agile, ready to adapt their strategies to successfully navigate the complexities of modern financial markets.

In this complete guide, we will delve deep into every aspect crucial for both novice and seasoned investors aiming to harness the power of these assets for wealth building. You will discover:

- What are income-producing assets

- Their role in portfolio diversification

- How to mitigate risks while optimizing returns

- Risks and rewards associated with different types of income-producing assets, from traditional stocks and bonds to alternative assets such as online businesses

- Shredded asset classes and their unique characteristics, advantages, and disadvantages

- Practical advice on constructing a robust portfolio of income-producing assets tailored to your financial goals, risk tolerance, and market conditions

- Essential strategies for avoiding common pitfalls and mistakes

- Real-world case studies

- Step-by-step instructions on how to get started with investing in income-producing assets.

Through this journey, you’ll gain the knowledge and confidence needed to build a portfolio that grows in value and generates a steady stream of income.

Part 1: Understanding The Spectrum of Income

In personal finance and wealth building, income is not just a singular concept but a spectrum, categorized chiefly into active, passive, and portfolio income. Understanding the differences between these types can significantly impact your investment strategies and financial planning.

Active Income: Hands-on Approach

Active income is earnings derived from direct involvement in activities or jobs. This includes but is not limited to wages, salaries, tips, commissions, and business income, where there is a significant degree of material participation.

Material participation, as defined by the Internal Revenue Service (IRS), requires that individuals meet specific criteria, such as working over 500 hours in the business during the fiscal year, performing the majority of the work in the business, working more than 100 hours with no other person working more, or materially participating in the activity in any five of the last ten years.

Active income emphasizes the necessity for personal effort and direct participation in earning activities. It’s the antithesis of earning money passively; your presence and active engagement are crucial.

It can be related to professional services, such as legal services, medical practices, or consultancy, where roles require not only extensive training and expertise but also personal involvement in service delivery; or it can be related to creative and performing arts, like artists, musicians, and actors who primarily earn active income through performances, exhibitions, and sales of artworks, which involve personal creation and presentation efforts.

You can find three types of active income:

- Salaries and Wages: The most prevalent form of active income, derived from regular job payments, demanding direct involvement and time. This category is exemplified by jobs like software developers ($109,020), registered nurses ($77,600), and high school teachers ($61,820).

- Self-Employment: Encompasses earnings from consulting, freelance work, and other personal business ventures, emphasizing the importance of understanding self-employment taxes and managing income variability.

- Commissions and Bonuses: Additional earnings based on personal achievements in sales or project completion, with the amount varying according to individual productivity and success.

Passive Income: Almost Effortless Earnings

In contrast, passive income, often considered unearned income, is money earned with minimal labor or active involvement. It’s the set-it-and-forget-it of income types, allowing individuals to generate revenue without the daily grind.

Common sources include rental income from real estate or stocks and bonds, YouTube content revenue, affiliate marketing, and income from digital assets or online business investments that require little ongoing effort, among many more.

However, it should be noted that not all income from these sources is always passive. For example, rental income can be considered active if the person is significantly involved in managing the properties.

Passive income might require initial effort or investment, but it can provide long-term returns.

These passive income earnings are the most attractive because they require a low level of participation and bring extra security to your portfolio. They help you focus on your active income strategies by generating their own cash flow without you having to worry about it.

Creating a successful passive income stream demands an initial investment of time, effort, or capital and an understanding of the specific tax rules that apply. For example, the IRS requires that passive income activities meet certain criteria to be classified as such, which can affect the tax benefits associated with losses from these activities. Despite the allure of “setting and forgetting,” occasional monitoring and strategizing are crucial to maintaining and growing passive income streams over time.

Portfolio Income: Somewhere in the Middle?

Different from active income and passive income, portfolio income is somewhere in the middle, offering a unique blend of opportunities for investors seeking to enhance their financial portfolios.

At its core, portfolio income consists of dividends, interest, and capital gains, amongst others. Unlike wages or salaries, which are subject to both income tax and Social Security/Medicare contributions, portfolio income benefits from lower tax rates on dividends and capital gains without the burden of Social Security or Medicare taxes.

While passive income may require some initial effort but continues to provide earnings over time, like royalties or rental payments, portfolio income is strictly derived from investment earnings. It does not stem from active business operations or direct business involvement, making it a distinct category in its own right.

There are three key increasing portfolio income strategies:

- Purchasing High-Paying Dividend Stocks: Buying stocks with above-average dividends can boost portfolio income. Options include direct dividend payments or reinvestment through dividend reinvestment plans (DRIPs).

- Investing in Dividend Exchange-Traded Funds (ETFs): Selecting ETFs that track high-dividend-paying stocks, such as the Vanguard High Dividend Yield ETF, offers a cost-effective method to enhance portfolio income.

- Writing Options: Investors can earn option premiums as additional portfolio income by writing call options against stock holdings. This strategy involves selling call options with the agreement to sell shares at a predetermined price, receiving premiums while managing the obligation to sell if stock prices exceed the strike price at expiration. However, writing options can be a complex and risky strategy and may not be suitable for all investors.

What’s appealing about portfolio income is its potential to enhance financial stability through diversified income sources while enjoying a more advantageous tax position.

As investors navigate their financial journeys, understanding and leveraging portfolio income’s characteristics can provide a valuable middle ground in achieving a balanced and prosperous financial portfolio.

Incorporating income-producing assets into an investment portfolio isn’t merely about generating income; it’s about strategic portfolio management. A diversified portfolio that includes a mix of income-generating and growth-oriented assets can more effectively weather market uncertainties.

Here are five strategies that might help you with your first steps:

- Understand Your Risk Tolerance: Before diversifying, assess how much investment fluctuation you can comfortably handle. Higher risk tolerance might mean a portfolio with more stocks, whereas lower risk tolerance may favor bonds or cash equivalents.

- Asset Allocation: Diversify your investments across different asset classes—such as stocks, bonds, real estate, or digital assets—to minimize risks tied to any single area. Aim for assets that don’t move in tandem during different economic conditions.

- Diversify Within Asset Classes: Go beyond broad asset categories by investing in various sectors and companies of different sizes within the stock market, for example. This helps shield your portfolio from downturns in any single sector or company.

- Geographical Diversification: Spread your investments across different regions and countries to mitigate risks associated with any particular national economy. This strategy can protect against local economic downturns by leveraging growth in other regions.

- Regular Rebalancing: Monitor and adjust your portfolio to maintain its original risk and return profile. This might mean selling assets that have gained value and buying more of those that have declined.

Part 2: Types of Income-producing assets

1. Online Businesses

Traditional businesses vs. online businesses

The distinction between traditional and online businesses is becoming increasingly pronounced, offering investors distinct pathways to generating income.

Traditional businesses often rely on physical assets, face-to-face interactions, and localized markets. Geographical boundaries and higher operational costs, including rent, utilities, and staffing, can limit these enterprises.

On the contrary, online businesses break free from these matters, leveraging the digital landscape to reach a global audience, minimize overhead, and enhance scalability.

Online businesses harness the power of the Internet to operate across global markets without needing physical premises. This virtual model significantly reduces overhead costs and allows for greater flexibility in managing operations.

Additionally, online enterprises have a notable advantage in terms of scalability. Digital platforms, whether content websites, e-commerce stores, or SaaS (Software as a Service) solutions, can often expand their reach and operations more swiftly than traditional businesses.

The digital marketplace also facilitates a unique capacity for automation and integration of advanced technologies like AI and data analytics, enabling online businesses to optimize operations and personalize customer experiences more effectively. This digital leverage is a crucial element in driving the growth and profitability of online enterprises.

Online businesses growth

Through the years—and especially during and after the global pandemic—online businesses have had more and more presence among markets.

Let’s take the SaaS industry as an example. The SaaS industry is expanding and impacting global business operations, collaboration, and competition. The industry is at the beginning of a growth phase with expected transformative developments.

As of 2022, the global SaaS market size was approximately $257.47 billion. From 2023 to 2030, the SaaS market is expected to grow at a CAGR of 19.7%, adding about $1,298.92 billion in value. The adoption of public and hybrid cloud solutions, integration of SaaS with other technologies, and the utilization of centralized, data-driven analytics are key factors driving growth within the industry.

Digital commerce has become a top choice for businesses to boost their sales and marketing strategies. This is because SaaS products significantly lower customer acquisition costs—how much an organization spends to acquire new customers—and enhance brand credibility.

E-commerce isn’t the exception regarding growth; it hasn’t stopped since its inception with CompuServe in 1969, and technological changes and global circumstances have accelerated this process. Online retail sales are projected to be 22% of global retail sales by 2023, up from 14.1% in 2019, and this year, over half of all ecommerce payments are expected to be made through digital wallets.

The pie chart below shows how Amazon was predicted to account for 39.5% of US retail e-commerce sales in 2022.

Let’s review some interesting facts and statistics about online business growth:

- 99.9% of US employers are small business owners; 92% value websites as crucial for digital marketing.

- 60% of adult Americans prefer not to shop in crowded malls, and 71% believe online deals are better.

- 1.79 billion people made online purchases last year.

- Online sales grew by more than 50% between 2013 and 2018 versus a 10% increase in offline sales.

- Businesses with blogs see 126% higher lead growth; blogs also boost website engagement significantly.

- Generation Z spends the highest percentage of their income online despite low incomes.

But, as usual, not all is perfect. There are some challenges to take into consideration when talking about online businesses:

- 80% of customers will stop business with a company after poor customer service experiences—this highlights the importance of effective customer service.

- 75% of clients expect online help within five minutes or they leave.

- 23% avoid websites due to cost, and 28% find them irrelevant.

- 35% of small businesses think they are too small for a website.

How online businesses serve as income-producing assets

Just like the online business market is growing as we’ve seen, so is the global online investment platform market, valued at $1.88 billion in 2021 and expected to grow at a CAGR of 13.9% from 2022 to 2030.

There has been a clear rise in online investors globally, and these platforms took the opportunity to reshape how individuals and institutions manage their investments. Investors are turning to online platforms driven by global connectivity and technological advancements.

The growing number of high-net-worth individuals and their interest in digital investments are significant growth factors. In the U.S. alone, the number of high-net-worth individuals grew by 13.5% in the previous year.

Investing in online businesses presents opportunities for both active and passive income streams. Active investors might engage in the day-to-day management of a website, constantly optimizing and expanding its operations. However, on the passive side, investors can benefit from models like fractional ownership, where they contribute capital but leave the management to experienced professionals. This can be particularly attractive for individuals who wish to benefit from the digital economy’s growth without engaging in the operational complexities.

Real-life success: A veteran investor’s perspective

To illustrate the effectiveness of investing passively with WebStreet, consider the experience of Chuck Mohler, a principal at Eagle Corporate Advisors. With a substantial background in business consulting, Chuck approached the digital investment realm with caution.

Chuck discovered WebStreet at a conference, sparking his interest due to its association with well-regarded entities in the online business marketplace. His approach involved proactive research and personal engagement, ensuring he fully understood the platform and its potential before investing.

The platform appealed to Chuck due to its emphasis on simplification, diversification, and trust in expert management. It offered a straightforward way to invest in multiple online businesses, handling the complexities of management and operation. Clearly, diversification across various digital assets provided a buffer against market volatility.

In summary, Chuck’s investment in WebStreet allowed him to diversify across multiple online businesses through a single platform, significantly easing the investment process and enhancing his trust due to the rigorous vetting process employed. The returns on his investments have aligned with, if not exceeded, his expectations, validating his decision to trust WebStreet’s model.

As you consider the steps to building and investing in a profitable online business, remember that the key to thriving in the e-commerce world is adaptability, continuous learning, and strategic foresight. Whether you choose to manage an online business directly or invest passively through WebStreet, the potential for significant financial success is substantial.

WebStreet simplifies the investment process, making it accessible and rewarding. With our platform, you’re not just investing; you’re setting the stage for a future of income growth and business success in the ever-expanding digital marketplace.

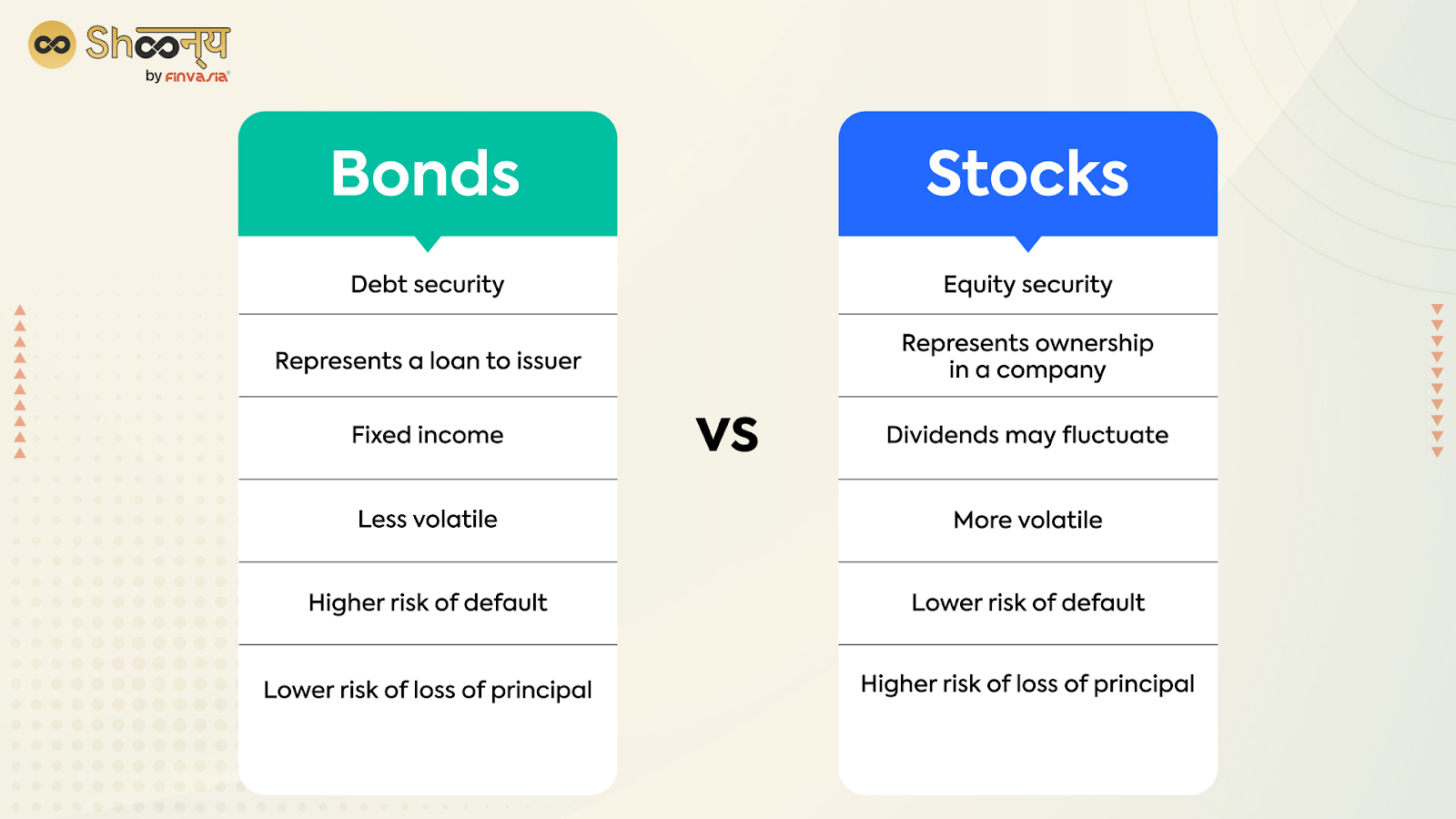

2. Stocks

Stocks represent ownership in a company, allowing investors to share in the profitability of businesses through mechanisms such as dividends. Dividends provide a stream of income that can grow over time and do not require substantial capital to start yielding benefits, making them accessible and attractive to many investors.

Stock valuation is a fundamental concept in investing that involves determining the current worth of a company’s shares. It is an essential process because it helps investors make informed decisions about which stocks to buy or sell based on their value rather than just price.

Stock valuation takes into account various factors, including a company’s financial condition, industry position, market environment, and potential for future growth. It is a critical process for assessing whether a stock is priced appropriately. It allows investors to identify investment opportunities where the market may not have fully recognized a company’s true value.

Several key valuation metrics are commonly used to measure and assess the value of a stock. Each metric provides different insights into a company’s financial health, growth prospects, and overall value, helping investors make more informed investment decisions. Here are some of the most important valuation metrics:

- Price-to-Earnings Ratio (P/E): This is one of the most widely used valuation metrics. It compares a company’s current share price to its per-share earnings. A high P/E ratio could indicate that a stock is overvalued or investors expect high future growth rates.

- Price-to-Book Ratio (P/B): The P/B ratio is essential for assessing a company’s intrinsic value relative to its market value. It is especially significant for financial firms like banks and insurance companies, where most assets and liabilities are constantly valued at market rates. For other companies, a P/B ratio below one can suggest that the company is undervalued or experiencing financial difficulties, whereas a higher P/B ratio might indicate potential overvaluation.

- Return on Equity (ROE): ROE measures a company’s ability to generate profits from its shareholders’ equity. It is a critical indicator of financial performance and managerial efficiency, showing how well a company uses investment funds to generate earnings growth. ROE is particularly valuable when comparing companies in the same industry, as it highlights the relative efficiency and profitability of competing businesses.

These metrics—P/E, P/B, and ROE—offer insights from different perspectives (earnings power, asset value, and investment return), providing a robust framework for evaluating the financial health and investment potential of a stock. Each metric covers a different aspect of a company’s financial status, making them collectively useful for a comprehensive assessment.

When considering stock investments, it’s crucial to understand the differences between purchasing individual stocks and investing in mutual funds:

- Individual stocks provide an opportunity to invest directly in specific companies, potentially allowing for targeted bets in certain industries. This approach can offer higher rewards but also comes with greater risk due to less diversification.

- Mutual funds invest in a collection of stocks across various companies, thereby spreading out investment risk through diversification.

If you’re looking to generate steady income, large-cap dividend stocks, often referred to as “Dividend Aristocrats,” are particularly appealing. These stocks are issued by blue-chip companies with a long history of increasing dividend payouts, providing both stability and reliable income. However, it’s important to note that some sectors, like technology and biotech, often do not offer dividends as these companies usually reinvest earnings back into growth and development.

Investors typically buy stocks for two main reasons: potential capital gains from price increases and earning dividends as investment income. For this, there are three types of stocks you can consider:

- Growth Stocks: These are companies with significant potential for future growth, often reinvesting profits for expansion, which is common in sectors like technology and biotech. Examples include Amazon and Nvidia.

- Value Stocks: These are stocks that trade at a price lower than their financial fundamentals suggest they should, potentially offering long-term profits. The Coca-Cola Company (KO) often exemplifies a value stock.

- Income Stocks: Stocks that provide steady dividend income, typically higher than guaranteed instruments like Treasury securities.

Smart investing involves understanding the potential of stocks to provide returns through growth, value appreciation, or dividends. Stocks like AT&T illustrate how investments can combine these elements, offering both capital gains and dividend income.

Some stocks might get more popular and can be sold for a higher price later (growth), some are cheaper than they should be and might go up in price (value), and some give you cash returns regularly (income).

3. Bonds

A bond is a debt security that functions as a loan between an investor and a borrower, which is typically a corporation or government. Bonds are a fundamental part of the financial markets used by various entities to finance projects and operations.

Bonds typically pay interest to investors at regular intervals, known as coupon payments, which are usually fixed but can also be variable depending on the bond type. The interest rate is determined at issuance and reflects the bond’s payment schedule and the issuer’s credit quality, which credit rating agencies assess.

Bonds are regarded as less risky than stocks, making them a popular option among investors seeking to generate regular income. They offer various maturity lengths, from a few months to several decades, allowing investors flexibility in managing their investment timelines. At the end of a bond’s term or maturity date, the issuer repays the investor its face value.

Additionally, bonds can be traded on the secondary market, offering liquidity to investors before maturity. Certain types of bonds, such as municipal bonds in the U.S., may also provide tax benefits, adding to their appeal.

Types of bonds

To better understand how bonds work and how we can leverage them, here’s an extended explanation of the different types of bonds available to investors:

- Corporate Bonds: These are issued by corporations to raise capital for various reasons, such as expanding operations, funding new projects, or refinancing existing debts. The risk and potential return on corporate bonds vary widely based on the creditworthiness of the issuing company. Investors should conduct thorough due diligence to assess the company’s financial health before investing.

- Treasury Bonds (T-Bonds): Issued by the U.S. government, Treasury bonds are considered among the safest investments since they are backed by the full faith and credit of the federal government. Treasury bonds have longer maturities, typically ranging from 10 to 30 years. Due to their low-risk nature, they offer lower yields compared to other bonds. Investors commonly use treasury bonds to preserve capital over the long term.

- International Government Bonds: These bonds are issued by foreign governments and allow investors to diversify their investment portfolios across different countries. They carry additional risks, such as political instability, currency fluctuation, and differences in economic growth rates. However, depending on the issuing country’s economic conditions, they may offer higher yields than domestic government bonds.

- Municipal Bonds: Often referred to as “munis,” these bonds are issued by state, city, or other local government entities to fund public projects like roads, schools, and infrastructure. Municipal bonds are particularly attractive to tax-conscious investors because the interest income is often exempt from federal income taxes and sometimes from US state sales tax and local taxes if the investor resides in the state where the bond is issued.

- Agency Bonds: These bonds are issued by government-sponsored enterprises (GSEs) or federal agencies. While not directly backed by the full faith and credit of the U.S. government, they still carry a high degree of safety. They are often used to fund specific activities like home mortgages or agriculture. Examples include bonds issued by Fannie Mae, Freddie Mac, and the Federal Farm Credit Banks.

Risk and returns of bond investing

As mentioned before, bonds are less risky because they usually come with a promise from the issuer to pay back the face value of the bond at its maturity. This means that unless the issuer defaults, investors receive their principal investment back. Stocks, on the other hand, provide no such promise.

Also, the bond market experiences less volatility compared to the stock market. Bonds generally have fewer and less severe price fluctuations, making them a safer investment, particularly in the short to medium term. Bond investors face less uncertainty about the day-to-day and month-to-month volatility in their investment’s value.

However, there are some risks associated with investing in bonds:

- Interest Rate Risk: Bond prices have an inverse relationship with interest rates. When interest rates rise, bond prices typically fall, and vice versa. This is because existing bonds with lower interest rates become less attractive than newly issued ones with higher rates.

- Reinvestment Risk: This occurs when bonds are callable, and interest rates have fallen. Issuers might redeem bonds early, forcing investors to reinvest the principal at lower rates than the original bonds, potentially reducing their income.

- Inflation Risk: If inflation rates increase faster than the income from bonds, the real returns on bonds can be negative, eroding purchasing power and effectively decreasing the investor’s real rate of return.

- Credit/Default Risk: Bonds are essentially loans that investors give to issuers, which could be corporations or governments. If an issuer defaults, investors may not get back their principal or interest, which makes understanding the issuer’s creditworthiness crucial.

- Rating Downgrades: If rating agencies downgrade a bond issuer, it can increase the cost of borrowing for the issuer and decrease the bond’s market value. This can negatively impact investors if they need to sell the bond before maturity.

- Liquidity Risk: Some bonds, especially corporate bonds, may have low liquidity, making them hard to sell quickly at a fair price. A thin market with few buyers can lead to significant price volatility and potential losses if the bond needs to be sold urgently.

These risks underscore the importance of due diligence and diversification when investing in bonds to mitigate potential negative impacts on investment returns.

4. Real Estate

Real estate assets represent a crucial component of many successful investment portfolios, offering the potential for both income and capital appreciation. Unlike stocks and bonds, real estate provides tangible assets, which can furnish investors with a unique mix of security, steady cash flow, and inflation hedging.

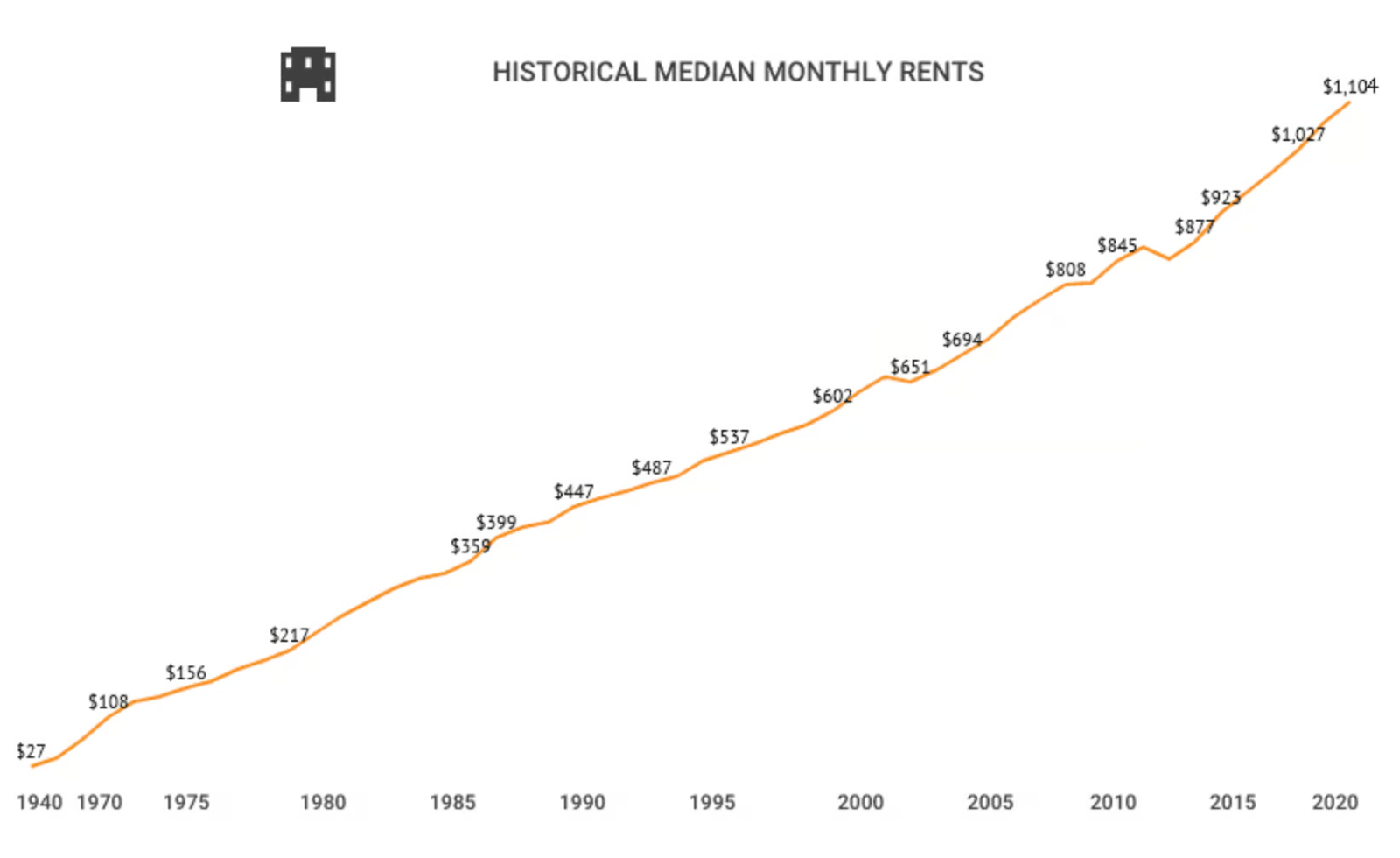

Rental properties are known for providing consistent and reliable returns, enhancing their appeal as a long-term investment strategy. Rental real estate typically outpaces inflation, ensuring that investment returns do not diminish in real terms. Historical data since 1980 shows an average annual rental rate growth of 8.86%, with some markets experiencing even higher growth.

Over the long term, real estate generally appreciates. The Case-Shiller Price Index reports a 333% increase in the median home price from 1987 to today, translating to an average annual increase of 9.7%. Ongoing high demand and a persistent housing shortage suggest that real estate prices may continue to rise, maintaining low vacancy rates and supporting rental growth.

As the chart shows, real estate investments have grown constantly over the years, fighting inflation while providing high returns.

Types of Real Estate Investments

Real estate investments come in various forms, each offering unique opportunities and challenges. Here are four primary types of real estate investments that cater to different investor needs and goals:

- Rental Properties: Investment in residential properties such as single-family homes, condos, or multi-family units where investors earn income primarily through renting out the property to tenants.

- Benefits: Provides steady, ongoing income through rent and potential appreciation in property value over time.

- Considerations: Requires active management, including maintenance and dealing with tenants, which can be mitigated through property management services.

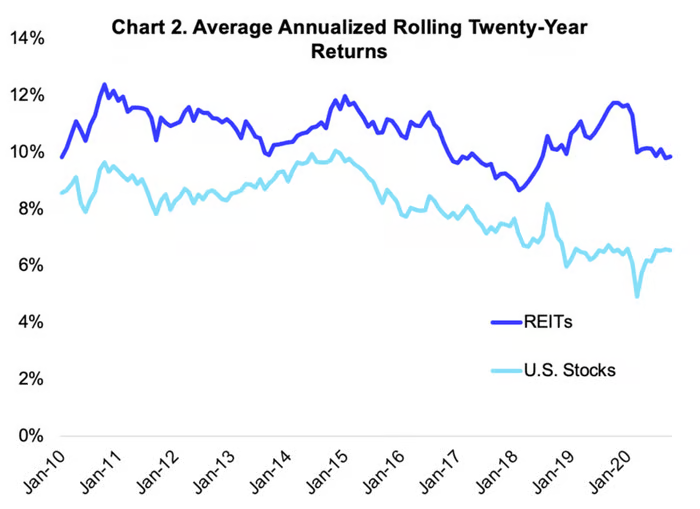

- Real Estate Investment Trusts (REITs): For those who prefer a more hands-off approach, REITs provide a way to invest in real estate without having to buy or manage the property directly. REITs are companies that own, operate, or finance the acquisition of real estate and distribute most of their income as dividends to shareholders.

- Benefits: Offers high liquidity compared to physical real estate, regular income through dividends, and diversification within the real estate sector. In fact, the National Association of Real Estate Investment Trusts says that 56% of the time, REITs outperformed the S&P 500 on an annual basis. This statistic indicates that REITs, more than half of the time, provided better yearly investment returns than the broader stock market, as represented by the S&P 500. Considering the simplicity and accessibility of purchasing shares in REITs, they continue to be one of the most effective ways for investors to begin investing in real estate today.

- Considerations: Publicly traded REITs can be subject to market fluctuations similar to stocks, which can affect their price and dividends.

- Commercial Real Estate: Investing in commercial real estate involves properties used solely for business purposes, such as office buildings, shopping centers, and hotels. These investments often come with longer lease agreements and can offer more stable rental income compared to residential properties. As of 2022, the commercial real estate market in the U.S. reached a revenue of $1.2 trillion, with shopping centers under construction accounting for 10.6 million square feet as of Q4 2022.

- Benefits: Commercial real estate tends to offer higher yields compared to residential real estate, often around 8-9% annually through rental income, plus potential property value appreciation. Also, inflation-linked rent escalations (e.g., 5% annually or 15% every three years) help safeguard against inflation, maintaining real rates of return.

- Considerations: Commercial real estate often requires a larger initial investment and can be more sensitive to economic conditions than residential real estate. Changes in interest rates, economic conditions, and demographic trends heavily influence it.

- Crowdfunding Real Estate Platforms: These platforms allow investors to pool money together to invest in a variety of real estate projects, from new developments to large-scale renovations. Crowdfunding makes it possible for non-accredited investors to participate in real estate ventures with a much lower financial entry point compared to traditional real estate transactions, often starting at about $1,000. It’s a growing industry, showing anticipated results of reaching 2724.7 billion dollars by the end of 2036, with a 50.1% CAGR growth rate from 2024 to 2036.

- Benefits: Lower barriers to entry compared to traditional real estate investments and the ability to invest in high-quality projects that may have been previously inaccessible. Investors also benefit from quicker engagement with potential returns on investments, as some properties come with tenants already in place, enabling rapid generation of rental income.

- Considerations: This option can carry higher risks and less liquidity, with restrictions on early withdrawal, potentially requiring investors to sell at a discount or incur penalties. The investment is typically locked in for a period of time, and the return can depend heavily on the platform and market conditions. Market volatility can affect property values and rental rates, potentially reducing returns if investments are timed poorly.

Each type of real estate investment has its own dynamics and requires different levels of capital commitment and involvement. Choosing the right type depends on an investor’s financial goals, risk tolerance, and investment strategy. It’s always best to remember the importance of due diligence and understanding the terms and conditions before committing to real estate investments or any investment at all.

Whether you’re looking for direct control and involvement in property management through owning rental properties or prefer a more hands-off approach via REITs or crowdfunding platforms, real estate offers diverse opportunities to enhance and diversify an investment portfolio.

Strategies for Success in Real Estate Investing

Achieving success in real estate investing requires a combination of strategic planning, detailed research, and effective management. Below are refined strategies to guide investors in navigating this complex market:

- In-depth Market Research: Conduct thorough research to understand local and global market trends. This includes analyzing demographic shifts, economic developments, and fluctuations in property demand. Utilizing advanced data analytics and demographic studies will provide insights into potential growth areas, helping to identify undervalued assets and avoid investment pitfalls.

- Comprehensive Financial Analysis: Perform detailed assessments of potential returns on investment. This involves cash flow analysis and evaluating the financial health of investments to ensure profitability and sustainability. Tools like AI-powered analysis can enhance decision-making by providing deeper insights into market conditions and investment viability.

- Proactive Property Management: Manage properties efficiently, either personally or through professional property managers. Effective management is crucial for maintaining property value, ensuring tenant satisfaction, and smoothing operational aspects of property ownership.

- Strategic Diversification: Diversify your investment portfolio across different types of properties and geographical areas to spread risk and capitalize on various market dynamics. This approach helps balance the portfolio against potential market downturns and capture opportunities from different real estate segments.

- Technology Utilization: Leverage emerging technologies to streamline transactions, enhance transparency, and expand investment opportunities. Innovations like virtual property tours, blockchain for secure transactions, and AI for market analysis can significantly improve efficiency and investor confidence.

- Networking and Relationships: Build and maintain strong relationships with industry experts. These relationships can open up new opportunities and offer deeper market insights. Networking can also provide access to privileged investment deals and partnerships.

- Adaptation to Emerging Trends: Stay updated with the latest industry trends, such as the rise of co-living spaces, the increasing demand for industrial real estate due to e-commerce growth, and the push towards sustainable building practices. Adapting to these trends will allow you to exploit new market opportunities.

5. Farmland: A Durable Income-Producing Asset

Introduction to Farmland Investing

Farmland has long been recognized as a vital component of America’s agricultural landscape, covering approximately 911 million acres across the country. As of recent reports by the U.S. Department of Agriculture (USDA), farmers and ranchers own about 61% of this land, with the remaining being held by investor groups and non-operating individuals.

This diversification in ownership underscores a growing trend: farmland is increasingly seen not just as a means of production but as a valuable investment asset. Historically reserved for those with direct ties to agriculture, the past few decades have seen farmland emerge as a sought-after component in diversified investment portfolios. The beauty of farmland as an investment lies in its dual capacity to generate stable rental income through cash rents and consistent appreciation in land value over time.

The rising interest in farmland investment is fueled by several factors. Firstly, it represents a tangible asset that provides inherent value as a resource essential for food production. Secondly, farmland offers a hedge against inflation and economic volatility, traits particularly appealing in uncertain economic climates. As global population growth continues to escalate demand for food production, the strategic importance and value of agricultural land are poised to increase.

As we delve deeper into the mechanics of farmland investment, prospective investors will find that this asset class not only offers a refuge from market turbulence but also a proven track record of robust financial performance.

Why invest in farmland?

Investing in farmland is increasingly recognized as a strategic move within the investment community, offering multiple benefits and serving as a safeguard against various economic pressures. Let’s review some key reasons why investors are turning their attention to farmland:

- Rising demand for food: The global population is projected to exceed 10 billion by 2050, significantly increasing the demand for food. The Food and Agriculture Organization (FAO) estimates that food production must increase by approximately 70% to meet this demand. This surge necessitates expanded agricultural production, which in turn boosts the value and utility of farmland. The rise of the middle class globally will further accelerate this demand as dietary preferences shift and overall food consumption increases.

- Finite supply: Farmland is a limited resource; they aren’t making any more of it. According to the American Farmland Trust, the U.S. loses almost 2,000 acres of farmland daily to development, summing up to around 500,000 acres annually. As available farmland becomes scarcer, its value and the strategic advantage of owning such land increase.

- Stable & long-term investment: Farmland has historically provided stable returns over long periods. The National Council of Real Estate Investment Fiduciaries (NCREIF) reports that farmland has had positive returns every year since 1991. Although the market for commodities may fluctuate, the underlying value of farmland tends to grow steadily. This makes it a less volatile investment than many traditional stocks or even some real estate investments.

- Diversification & low correlation: Investing in farmland allows for diversification across different types of crops and geographies, thereby spreading risk. Diversification is the cornerstone of a robust investment portfolio, and farmland offers significant diversification benefits due to its low correlation with traditional asset classes like stocks and bonds. Historical data often demonstrates that farmland returns have little to no correlation with broader market movements, making it an excellent hedge against market volatility and economic downturns. Different crops and locations further help hedge against localized economic downturns, pests, and adverse weather conditions.

- Sustainability and organic production: The demand for organic products has been growing, with the Organic Trade Association reporting that organic food sales in the U.S. exceeded $50 billion in 2019. Investing in organic farmland taps into this high-demand sector, though it requires careful selection of suitable locations and soil types.

- Tax benefits: Farmland owners can benefit from various tax advantages. For example, depreciation for specialized crops—such as grapes, fruit, and nut trees—reducing gross income for tax purposes, conservation trusts and easements, and agricultural land benefits from lower property tax rates in many states—a policy designed to support farming activities.

- Inflation Hedge: As a tangible asset, farmland benefits from inflation. Historical data shows that as commodity prices rise, so does the income potential from farmland and its overall value. This relationship makes farmland an effective hedge against inflation.

- Passive Income Potential: Farmland can generate income through cash rent payments or through sharecropping agreements, providing owners with a passive income stream while benefiting from the appreciation of the land itself.

- Proven Track Record of Appreciation: Farmland has shown significant appreciation over the past decades. For instance, the USDA and other reports show the average value of farm real estate (land and buildings on farms) has increased consistently, underlining farmland’s potential as a long-term investment.

The flow chart below shows US’ (in light blue) and Kentucky’s (in blue) farmland value appreciation from 2000 to 2023.

As we understand, investments are more attractive when their value increases over time, when they keep pace with inflation, and when their volatility is low. Farmland seems to have it all, different than stocks or real estate—which suffer from high volatility, or bonds—which typically fail to hedge against inflation effectively. Farmland generally maintains steady appreciation and is less susceptible to economic fluctuations.

Moreover, while stocks and real estate markets may crash, farmland continues to hold intrinsic value due to its finite supply and essential role in global food supply, making it a robust investment choice for those looking to stabilize and diversify their portfolios.

Expected returns from farmland

Investing in farmland is often seen as a conservative, long-term investment strategy. It’s crucial to adopt this mindset as the value and returns from farmland accumulate over time, reflecting the gradual appreciation of the land and the income derived from agricultural production. But what can you expect from investing in farmland?

- Long-term appreciation and stability: Farmland is a hold asset, with its value generally increasing over time. Historical trends have shown that farmland not only appreciates but also maintains this appreciation consistently. For instance, in the last two years alone, there has been a significant appreciation, approximately 42%, in farmland values. This steady rise is attributed to the decreasing availability of arable land, coupled with increasing demands from a growing global population and expanding economic developments.

- Annual return expectations: While short-term returns can be attractive, farmland should primarily be viewed through the lens of long-term investment. Historically, the average annual return on farmland has been around 12.8%, as noted by platforms like AcreTrader. However, it’s also common for more modest expectations, with annual returns averaging around 2.5% in some cases, reflecting the stable yet slower-growing nature of this asset class compared to more volatile markets like stocks.

Source: https://acretrader.com/resources/farmland-values/farmland-returns

- Impact of economic and environmental factors: Investing in farmland is not without its risks. Factors such as changes in commodity prices, interest rates, and government agricultural policies can significantly impact earnings from farmland. Additionally, environmental factors such as droughts or floods pose risks to crop production, potentially affecting both short-term income and long-term land values.

Investing in farmland is a strategic decision that requires patience and a long-term perspective. While the asset class does not promise quick gains, its strength lies in stable growth, resilience against inflation, and low correlation with other investment categories, making it an attractive option for those looking to diversify their investment portfolios and secure steady, long-term returns. Investors are encouraged to conduct thorough due diligence and consider both the immediate and future potential of farmland before committing to this type of investment.

How to invest in farmland

Farmland investing has evolved over the years, offering a variety of entry points for investors of all types. Whether you’re looking to dive directly into owning land or prefer a hands-off approach, there are multiple strategies to consider:

- Owning land directly: Direct ownership of farmland remains a viable option for those looking to make a substantial investment in real estate. By purchasing land outright, you can lease it to farmers for crop production or livestock raising, functioning similarly to a rental property investment. The financial commitment for direct land ownership is considerable. Based on USDA data from 2022, the average cost per acre was $3,800. For a typical farm of 445 acres, this equates to an investment of approximately $1.69 million. However, smaller or less expensive plots may provide a more accessible entry point for new investors.

- Farmland REITs: Real Estate Investment Trusts (REITs) that specialize in farmland offer the benefits of real estate investment without the management burdens. Farmland REITs provide income through dividends and the potential for capital appreciation. Investing in farmland REITs offers liquidity, lower entry costs, and ease of diversification compared to direct ownership. Notable farmland REITs include Gladstone Land (LAND) and Farmland Partners (FPI), which distribute a significant portion of their income to shareholders.

- Agricultural stocks: For those not ready to invest directly in land, agricultural stocks are an alternative. These stocks represent companies involved in various facets of agriculture, from crop production to equipment manufacturing. Key players in the agricultural stock market include Archer-Daniels-Midland (ADM), Corteva (CTVA), and Scotts Miracle-Gro (SMG). These companies benefit from both the operational aspects of agriculture and the underlying value of any owned farmland.

- Farmland mutual funds and ETFs: Mutual funds and ETFs with a focus on agriculture allow investors to pool their money into a diversified portfolio related to farming and agricultural productivity. An example is the Fidelity Agricultural Productivity Fund (FARMX), which invests predominantly in companies that enhance agricultural efficiency. However, potential investors should be aware of the fees associated with mutual funds, which can impact overall returns.

- Crowdfunding platforms: Crowdfunding platforms like AcreTrader and FarmTogether make it possible to invest in farmland with significantly less capital. These platforms enable investors to purchase shares of specific farmland projects, reducing the financial barrier to entry.

Previously, investing in farmland typically meant buying a whole farm—a costly and knowledge-intensive endeavor. Today, investors have a broader range of options to include farmland in their portfolios, from buying land directly to investing in farmland-focused REITs, stocks, mutual funds, and innovative crowdfunding platforms.

Each method comes with its own set of advantages, challenges, and risk profiles, making it crucial for potential investors to carefully consider their financial goals, risk tolerance, and investment timeframe before choosing the path that best suits their needs.

6. CDs/Money Market Funds

Certificates of Deposit (CDs) and Money Market Funds are two popular types of investment vehicles that cater primarily to conservative investors looking for safety and liquidity.

Certificates of Deposits are special types of savings accounts offered by banks and credit unions that involve locking funds for a fixed period, during which they accrue interest at a predetermined rate. Unlike regular savings accounts, withdrawing funds from a CD before the maturity date incurs penalties—you may have to forfeit a portion of your accrued interest—though they compensate by typically offering higher interest rates. CDs provide a predictable, secure investment option without the volatility of the stock market, making them an excellent choice for risk-averse investors.

Money Market Funds are mutual funds that invest in highly liquid, short-term debt securities such as U.S. Treasuries, commercial paper, and certificates of deposit. These funds aim to offer investors a safe place to invest easily accessible cash-equivalent assets that are more profitable than traditional savings accounts but still very low risk. Unlike money market accounts (MMAs) offered by banks, money market funds are investment products and do not come with FDIC insurance, though they strive to maintain a stable $1 per share NAV (net asset value).

Both investment vehicles provide valuable options for those looking to preserve capital while earning returns that are competitive with other low-risk investments. They are particularly appealing during times of economic uncertainty or when investors seek to balance out more volatile investment holdings with safer assets.

Comparing risks and returns

CDs and Money Market Funds offer appealing low-risk investment opportunities but differ in their risk profiles and potential returns. This section aims to compare both the risks and returns of each one to help you make informed choices based on your financial goals and risk tolerance.

Risks of CDs:

- Guaranteed returns: CDs offer fixed interest rates, which means the return is predictable and guaranteed for the term of the CD. This makes the investment way less risky.

- Insured investments: The FDIC or NCUA protects up to $250,000 per depositor per institution, minimizing the risk of loss.

- Penalties for early withdrawal: Withdrawing funds from a CD before its maturity date can result in penalties, which could eat into the interest earned.

- Interest rate risk: If interest rates rise after you purchase a CD, you could miss out on higher earning opportunities elsewhere, as your funds are locked in at a lower rate. This is known as opportunity cost.

Returns of CDs:

- Fixed interest rate: The interest rate on a fixed-rate CD remains constant throughout the term, providing a stable and predictable return. Depending on the terms, the interest rates can be quite competitive, especially for longer durations.

- Higher rates for longer terms: Typically, the longer the investment period, the higher the interest rate you’ll earn, which can significantly enhance the growth of your investment over time.

- Returns aren’t as high as other investments: Unlike the stock market, investing money in CDs usually brings less returns than this first one.

Risks of Money Market Funds:

- Variable Returns: Returns are based on the current interest rates, which can fluctuate, leading to variable income from these investments. Factors such as changes in the federal funds rate or economic downturns can more significantly impact MMFs than CDs due to their reliance on current market conditions.

- Low credit risk: Investments are in high-quality, short-term debt instruments, which traditionally have a low risk of default.

- Liquidity risk: While generally liquid, certain market conditions could affect the ease of withdrawing funds without impacting the NAV.

- No FDIC insurance: Unlike bank money market accounts, money market funds are not insured by the FDIC, adding a layer of risk.

Returns of Money Market Funds:

- Variable interest rates: The interest paid on a money market fund can fluctuate daily and is influenced by changes in market interest rates.

- Potentially higher yields: Yields on money market funds may be slightly higher than those on savings or money market accounts, especially during periods of higher interest rates.

When deciding between these two types of investments, consider your need for liquidity and your risk tolerance. Money market funds might be preferable if you require quick access to your funds or if you anticipate needing to adjust your investment in response to changing economic conditions. On the other hand, CDs are an excellent choice if you can commit your funds for a longer period and are seeking a guaranteed return.

7. Royalties

Royalties must not be confused with Intellectual Property, even though they are connected.

Intellectual Property (IP) refers to creations of the mind, such as inventions, literary and artistic works, designs, symbols, names, and images used in commerce. IP is legally recognized and provides its creators or owners with exclusive rights to use their creations for a certain period of time. You own the idea.

Royalties, on the other hand, are the actual financial compensation paid to the holders of intellectual property for others’ use of their IP. Essentially, royalties are a way for IP owners to monetize their creations. When someone uses the IP—whether by publishing a book, playing a song, manufacturing a patented product, or broadcasting a film—they pay a royalty to the owner or creator.

For instance, a musician who writes a song will own the copyright. When others want to perform or reproduce it, they must pay royalties to the musician. Similarly, inventors who hold patents can earn royalties when companies license their patented technology to produce or sell products.

Common types of royalties include:

- Book royalties: Paid to authors by publishers based on book sales.

- Performance royalties: Paid to musicians for using their music on platforms like radio and in public performances.

- Patent royalties: Paid to inventors by third parties using their patented technology.

- Franchise royalties: Paid by franchisees to franchisors for the rights to operate under a brand name.

- Mineral royalties: Paid to landowners by extractors of natural resources like oil and minerals.

Investing in royalties can be an attractive option for those looking to generate passive income from various types of intellectual property, creative works, or natural resources; it’s a highly attractive option for investors looking to protect their money while maximizing overall returns. You can enjoy uncorrelated assets—like music royalties, which perform independently of public markets—a competitive yield—with a track record of strong earnings and the potential to deliver double-digit yields— and passive income.

Pros and cons of investing in royalties

Royalties represent a unique form of investment integral to generating income from creative and intellectual properties. While they offer distinct benefits, potential investors should also know their limitations. Here are some pros and cons for you to consider:

Pros of Investing in Royalties

- Steady income stream: Royalties can provide a consistent source of income over an extended period. This is particularly beneficial for long-term financial planning as it offers regular returns from works that continue to be consumed, such as music tracks, books, or patented technologies.

- Passive income: Once the initial deal is set, royalties can generate income without ongoing effort from the investor. This passive income allows for earning while focusing on other investments or projects.

- Income diversification: Adding royalties to an investment portfolio can help diversify income sources. This diversification can reduce the risk of relying solely on more volatile investments like stocks or real estate.

These are the three main qualities that a passive investor would desire: long-term growth, low risk, and steady, hands-off income. However, there are also downsides:

- Lack of control: Investors typically have little control over how the creative work is managed or exploited once they invest in royalties. Changes or updates to the work, such as new editions or adaptations, usually require approval from other rights holders.

- Uncertainty of income: The income from royalties can be unpredictable. Factors such as changes in public interest, market trends, or the emergence of new technologies can impact the popularity and, consequently, the royalties earned from an asset.

- Potentially low returns: Not all royalty agreements result in high returns. The success of a royalty-generating asset often depends on its popularity and market reach. For instance, a book or a music album might not perform as expected, leading to minimal royalty payments.

While royalties can offer a lucrative and steady income stream, the investment comes with its challenges. As an investor, you should carefully evaluate your investment goals and risk tolerance when considering royalties as part of your broader investment strategy and implement due diligence for better results.

How to Invest in Royalties

For portfolio diversification enthusiasts and steady income seekers, investing in royalties is definitely an appealing strategy. There are several ways to invest in royalty investments, each offering different opportunities and benefits:

- Royalty Trusts: Royalty trusts are publicly traded entities that invest in producing assets such as oil, gas, and minerals. They are an accessible option for individual investors to enter the royalty market. These trusts acquire ownership of rights to resource leases and deposits, and the income generated from these assets is distributed to shareholders in the form of dividends. A significant benefit of investing in royalty trusts is their tax efficiency; they typically distribute 90% of their income as dividends, which are taxed at the shareholder’s personal income tax rate rather than corporate rates.

- Royalty auctions: Investors can also participate in royalty auctions through various online platforms. These auctions allow you to bid on and purchase royalty interests in different types of assets, including music tracks, patents, and mineral rights. Platforms like Songvest specialize in music royalties, while EnergyNet focuses on oil and gas royalties. Royalty Exchange offers a broad spectrum of royalties, including those from movies, TV shows, and other media. This method enables investors to acquire direct stakes in specific royalty streams, offering potentially high returns based on the asset’s performance.

- Direct investment: Another method is direct investment in royalties by negotiating directly with the rights holder to purchase a stake in the future revenue of a creative work, patent, or other asset that generates royalties. This requires more substantial upfront investment and due diligence but can result in significant long-term returns.

Visit our insights page to learn more about how to diversify your portfolio with online businesses, or follow along as we acquire them, manage them, and then sell them.

Part 3: Building Your Income-Producing Assets Portfolio

Creating a diversified portfolio of income-producing assets is an effective strategy to secure a reliable income stream, diversify your financial portfolio, and ultimately achieve financial freedom. A diversified portfolio can also be understood as an investment portfolio, a collection of assets you buy or deposit money into to generate income, with the difference that these ones usually don’t provide regular income.

Whether you are an experienced investor or just starting, understanding how to build a robust assets portfolio is crucial.

Here’s a step-by-step guide to building one that can include income-generating assets:

A. Start With Your Goals and Time Horizon

When creating a diversified portfolio of income-producing assets, the first step is to clearly define your financial goals and understand your investment time horizon. A time horizon is crucial as it influences the type of investments you should consider, which ones to avoid, and the appropriate duration to hold these investments.

- Short-term goals (within 12 months): For objectives less than five years away, such as saving for a down payment on a home or funding a major purchase, it’s wise to prioritize capital preservation. Investments less affected by market volatility, such as money market funds or short-term certificates of deposit, are more suitable as they offer liquidity and safety.

- Medium-term goals (1-5 years): Goals set for an intermediate term, like purchasing a property or funding a child’s education within the next decade, allow for slightly more risk. This period is adequate for recovering from market fluctuations. Hence a balanced mix of stocks and bonds through vehicles like balanced mutual funds is beneficial.

- Long-term goals (more than 5 years): Long-term goals such as retirement require investments that can yield higher returns despite higher risks. Stocks and equity funds are suitable for this time frame since the potential for higher returns outweighs short-term volatility, and there is ample time to recover from any downturns.

Understanding your time horizon not only helps in selecting the right investment vehicles but also in managing risk effectively.

B. Evaluate the Risk vs. Reward of Income Producing Investments

When considering income-producing assets, investors must critically evaluate the balance between risk and reward to determine the potential success of each investment relative to the investor’s financial goals and risk tolerance.

Therefore, it’s mandatory to explore key factors and strategies to effectively analyze and manage the risk-reward ratio in income-producing investments. We can review them:

- Risk Assessment: Understanding the specific risks associated with different types of income-producing assets is crucial. For example, real estate investments may offer stable returns but can be affected by market fluctuations and property management challenges. On the other hand, stocks might provide high returns but are susceptible to market volatility and economic downturns. Assessing these risks involves analyzing historical data, market trends, and economic forecasts to gauge potential impacts on investment returns.

- Reward Potential: The attractiveness of an income-producing asset is often measured by its potential to deliver steady, predictable returns. For instance, dividend-paying stocks or real estate investment trusts (REITs) can offer regular income streams, appealing to those seeking to supplement their earnings or stabilize their investment portfolios. Evaluating the reward potential requires understanding the asset’s yield history, the stability of income generation, and the growth potential of the underlying investment.

- Risk-Return Trade-off: Every investment decision involves a trade-off between risk and return. Higher returns often come with higher risks, so balancing these elements is key to achieving investment objectives. Investors should consider their personal risk tolerance and how much uncertainty they are willing to accept for potentially higher gains. This might mean choosing bonds or CDs for lower risk and stable returns, or venturing into more volatile markets like digital assets for higher growth potential.

- Diversification Strategies: Diversification is a fundamental risk management technique that involves spreading investments across various asset types, sectors, or geographical locations to mitigate potential losses. By diversifying, investors can protect themselves against significant fluctuations in any single investment area. This approach not only helps in managing risk but also in capitalizing on different growth opportunities across the investment spectrum.

- Periodic Review and Adjustment: Regularly reviewing and adjusting the investment portfolio is essential to align with changing market conditions and personal financial goals. This dynamic approach allows investors to take advantage of emerging opportunities and minimize losses by withdrawing from declining sectors or asset classes.

A great tool to use when evaluating the risks and returns of your investments is the risk/reward ratio, it quantifies the potential reward an investor can earn for every dollar risked. A lower risk/return ratio is often seen as preferable, indicating less risk for a potential gain. Ideally, many strategists suggest aiming for a ratio of at least 1:3, signifying three units of expected return for every unit of risk undertaken.

The risk/reward ratio is an invaluable tool for managing investment risk. It helps investors to make informed decisions by comparing potential losses with expected gains. Keep in mind it can evolve over time due to changing market dynamics or shifts in the underlying asset’s performance. Regular monitoring and adjustment of this ratio ensure that the investment continues to align with the investor’s goals and risk tolerance.

Another one is the PEG ratio, a valuation metric that evaluates the worth of a stock by looking at a company’s earnings growth rate and its price to earning ratio. While a low PEG indicates a stock may be undervalued, a high one says a stock may be overpriced. This highly helps you make informed decisions.

Evaluating risk versus reward in income-producing investments requires a detailed and informed analysis. By understanding the inherent risks, assessing potential rewards, and employing diversification and regular portfolio adjustments, investors can strategically navigate the complexities of the financial markets.

This balanced approach aims to optimize returns while minimizing risks, aligning with the investor’s long-term financial objectives and risk tolerance levels

C. Understand Your Risk Tolerance

Determining your risk tolerance is pivotal in building a portfolio of income-producing assets. It involves your financial capacity to handle potential losses and your psychological comfort level with the inherent risks associated with different types of investments.

Whether you view market downturns with anxiety or see them as opportunities, your feelings about risk play a crucial role in shaping your investment strategy. Reflect on past reactions to market declines or financial losses. Were these experiences distressing, or could you handle the volatility without stress? Your answers can guide the level of risk you’re comfortable taking.

Apart from psychological comfort, consider your financial ability to sustain losses. This involves evaluating your current financial obligations, such as mortgages, education expenses, or family care. Those with fewer financial burdens may have a higher capacity to endure market fluctuations than those with significant responsibilities.

Life events or changes in your personal life, such as receiving a windfall or experiencing a job loss, can affect your ability to take on risk. Such events may necessitate reassessing your investment approach to either scale back or potentially increase risk, depending on the new circumstances.

The risk versus time horizon—the duration you plan to invest significantly influences your risk tolerance. Longer investment periods typically allow for a higher risk tolerance since there is more time to recover from market dips. As you approach the end of your investment horizon, transitioning to more conservative investments can help preserve capital.

Understanding these facets of risk tolerance can help you create an investment strategy that aims for optimal returns and aligns with your personal comfort level and financial goals. This alignment is crucial to maintaining a strategy you can commit to over the long term, minimizing the likelihood of making impulsive decisions during volatile periods.

D. Choose Your Investment

When building your portfolio of income-producing assets, selecting the right investments is crucial to achieving the desired results. One of the most-known strategies is diversifying across asset classes. Diversification not only manages risk but also enhances potential returns.

Nobel Prize-winning economist Harry Markowitz described diversification as “the only free lunch in finance,” meaning you can achieve better returns without additional risk by diversifying your investments. For instance, splitting your investment between different assets like the S&P 500 and commodities can yield higher returns than investing in a single asset class.

This strategy should include a mix of traditional assets like stocks and bonds and alternative investments such as real estate or online businesses. If you’re looking for innovative investment avenues, WebStreet offers a unique platform for investing in online businesses, providing an opportunity for high returns and passive income through expertly managed portfolios.

Understand the 80/20 rule

The Pareto Principle, or the 80/20 Rule, suggests that 80% of outcomes come from 20% of all inputs. Apply this rule when picking your investments to focus on those that provide the majority of your portfolio’s returns. This approach helps streamline your investment efforts and concentrate on assets that significantly impact your portfolio’s performance.

Here’s how to effectively apply this rule to your investment approach:

- Identify High-Impact Investments: Focus on selecting the investments that have historically provided the majority of returns in your portfolio. This may mean prioritizing stocks that have shown strong performance or sectors that are fundamental to market growth.

- Efficiency in Resource Allocation: By applying the 80/20 rule, allocate more resources and time to managing and researching the 20% of your assets expected to yield 80% of the returns. This approach lets you concentrate on the most impactful assets, optimizing your investment efforts.

- Simplify Decision-Making: Simplify your investment choices by focusing on key performance indicators that significantly influence outcomes. This can mean investing in a few high-quality stocks or funds rather than spreading your investments thinly across too many options.

- Prioritize Based on Impact: Recognize and prioritize the parts of your portfolio that contribute most significantly to its overall performance. This could involve reallocating investments from underperforming assets to those within the 20% that drive 80% of your portfolio’s success.

Focusing on fewer, higher-impact investments can reduce transaction fees and time spent on portfolio management.

You should regularly review your portfolio to ensure that the 20% of assets you focus on continue to drive the majority of returns. Market conditions change, and yesterday’s high performers may not hold the same position tomorrow.

Important metrics when selecting investments

When selecting investments, consider dividends, P/E ratios, beta, EPS (Earnings Per Share), and historical returns. Expanding on the significance of various metrics used in evaluating investments can provide a deeper understanding of what to consider when selecting stocks or other securities. Here’s a more detailed look at each key metric:

- Dividends: Dividends are payments made to shareholders from a corporation’s earnings. They are a significant component of the total return on investments, often reflecting the company’s profitability and stability. Regular dividend payments are signs of a company’s good health and a reliable income stream for investors. Look for companies with a consistent history of paying dividends and the potential for dividend growth, which can indicate sound financial management and profitability.

- Price-to-earnings (P/E) Ratio: The P/E ratio is a key indicator of whether a stock is fairly valued compared to its earnings. It measures the market’s expectations of a stock, providing insight into whether it’s overvalued or undervalued. Compare the P/E ratios within the same industry for a better assessment. A high P/E might suggest that a stock is overpriced or indicate investors are expecting high growth rates in the future.

- Beta: Beta measures the volatility of a stock relative to the overall market. It helps investors understand the risk involved in holding a particular stock and how it might react to market movements. A beta greater than one suggests that the stock is more volatile than the market, offering potentially higher returns at increased risk. Conversely, a beta less than one indicates less volatility and typically less risk.

- Earnings per share (EPS): EPS is a direct reflection of a company’s profitability on a per-share basis, crucial for comparing the performance of companies within the same sector or industry. A higher EPS generally suggests a company is more profitable and has more funds available to return to shareholders. Observe the trend in EPS over several quarters to gauge whether the company’s profitability is improving, stable, or declining. Consider the quality of earnings as well—ensure they are not artificially inflated through accounting tricks.

- Historical Returns: Analyzing the historical returns of an investment can provide insights into its past performance and how it has reacted to different market conditions. This metric helps set expectations and assess the potential future performance of an investment. While historical performance is informative, it should not be the sole factor in investment decisions, as past returns do not guarantee future results. It’s crucial to consider current market conditions and future outlooks.

Carefully review them, some will resonate more than others, because in the end, you’re the only one who knows what’s best for you. These metrics offer a comprehensive view of potential investments, aiding in the construction of a diversified and resilient portfolio.

Technical vs. Fundamental Analysis

When building a diversified investment portfolio, understanding the methodologies for evaluating potential investments is crucial. Here are two main approaches: Technical Analysis and Fundamental Analysis.

- Fundamental Analysis: Assesses the intrinsic value of stocks by examining financial statements, economic indicators, company news, and more. This analysis aims to determine a security’s real worth. It uses financial statements like income statements, balance sheets, and cash flow statements to gauge a company’s financial health. Metrics like GDP growth and unemployment rates help assess the economic environment that could impact a company’s performance. Interest rates and other qualitative factors, such as market position or competitive advantage, are also considered. This analysis is best for long-term investors who are looking for sustainable performance and are less concerned with short-term fluctuations.

- Technical Analysis: Uses past market data like price and volume to predict future market behavior. This approach is based on the idea that market inefficiencies can be identified and exploited for profit. It uses mathematical calculations based on price, volume, and open interest that aim to predict future prices; looks at the amount of trading to interpret investor behavior and market trends; chart patterns; relative strength between assets; and general trend analysis. This approach is ideal for traders interested in short-term investments and those who prefer a more hands-on, data-driven approach to capitalize on market trends.

Many savvy investors combine both fundamental and technical analysis to enhance their investment strategy. This blended approach allows investors to understand the value of an asset and also to optimize the timing of their trades.

You can use fundamental analysis at the starting point of the investment to assess the asset’s intrinsic value and understanding its long-term prospects, and the technical analysis for refinement, to pinpoint the best times to enter or exit positions, maximizing potential returns and minimizing risks.

Balance and diversification

Deciding the mix between stocks and bonds is necessary. Historically, stocks have offered higher returns compared to bonds, albeit at a higher risk. Depending on your age and risk tolerance, balance your portfolio accordingly.

Younger investors might adopt a heavier stock allocation, while those nearing retirement might prefer the stability of bonds. Using a rule like the “120 rule” for a more balanced approach can help you. Subtracting your age from 120 can help determine the percentage of your portfolio that should be allocated to stocks.

Investing in a diversified portfolio is essential to maximize returns while minimizing risk. Diversification across different asset classes not only protects your assets but also enhances the potential for returns.

By spreading investments across various asset classes, sectors, and geographies, you mitigate the risk of significant losses. If you invest in both the technology sector and utilities, you can balance the high growth (but higher volatility) of tech stocks with the stability of utilities, which often provide consistent dividends.